TechVista Systems, a global provider of IT solutions, has successfully assisted Twenty-Two organizations with ensuring compliance with new value-added tax (VAT) regulations. VAT implementation was performed for clients that use Microsoft Dynamics 365, AX 2012, NAV 5, NAV 2013, GP 2013, and GP 2018. TechVista’s team implemented VAT ledgers, standard VAT inquiries, and reports, and updated vendor and customer master data with tax IDs. VAT codes were implemented for 5%, 0%, and exempt status, using all applicable jurisdictions, as well as VAT groups (reverse charge, standard rated, inter-company, exempted, zero-rated supplies, etc.). The team performed SQL collation for Arabic data, and also set up an FTA audit file and VAT return report according to UAE VAT requirements. “Over the past two months, we have partnered with several organizations in the UAE to make sure that their implementation of all VAT rules and regulations takes place smoothly and efficiently,” said Adeel Edhi, Vice President at TechVista Systems. “Our technical experts have successfully assisted our esteemed clients with full VAT compliance by updating their enterprise systems to automatically apply VAT and maintain multi-year tax records as required by the FTA.” The clients for whom VAT implementation was completed successfully include Albuainain Group KSA, ENOC, Dubai Autodrome, Fortes Holdings, Jumeirah International Nursery, Motor City, Sunmarke School, Tribe Fitness, Union Properties, and Uptown Mirdiff. With over 100 successful Enterprise and Corporate implementations and regional offices in the UAE, Oman, and Qatar, TechVista Systems brings value to companies of all sizes through its solutions and professional services. About TechVista Systems TechVista Systems is a Microsoft Gold partner delivering innovative business solutions in customer relationship management (CRM), enterprise resource planning (ERP) and digital marketing. As a leading technology provider with more than 3,000 employees around the world, we help our local and international customers maximize their IT investments that drive business results. We leverage our deep technical skills, accelerators, frameworks, products, best practices, and Microsoft domain expertise in provision of these solutions to help our customers achieve their business goals by gaining a competitive edge regardless of their local environment. Visit us on our website www.techvistasystems.com or email us at [email protected].

21 Comments

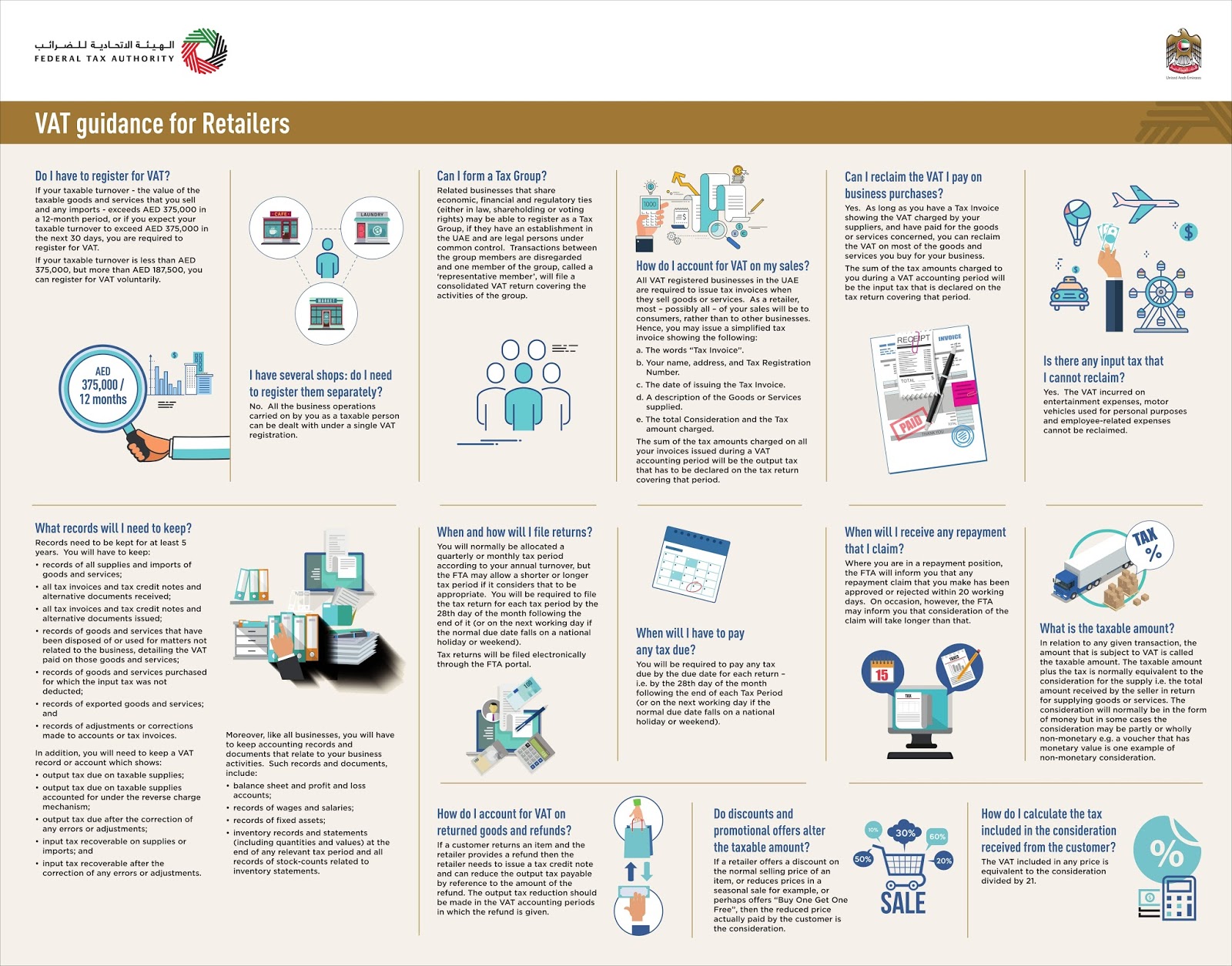

Value Added Tax (VAT) guidance for Retailers published on Federal Tax Authority website www.tax.gov.ae. Do I have to register for VAT? If your taxable turnover – the value of the taxable goods and services that you sell and any imports – exceeds AED 375,000 in a 12-month period, or if you expect your taxable turnover to exceed AED 375,000 in the next 30 days, you are required to register for VAT. If your taxable turnover is less than AED 375,000, but more than AED 187,500, you can register for VAT voluntarily. I have several shops: do I need to register them separately? No. All the business operations carried on by you as a taxable person can be dealt with under a single VAT registration. Can I form a Tax Group? Related businesses that share economic, financial and regulatory ties (either in law, shareholding or voting rights) may be able to register as a Tax Group if they have an establishment in the UAE and are legal persons under common control. Transactions between the group members are disregarded and one member of the group called a ‘representative member’, will file a consolidated VAT return covering the activities of the group. How do I account for VAT on my sales? All VAT registered businesses in the UAE are required to issue tax invoices when they sell goods or services. As a retailer, most – possibly all – of your sales will be to consumers, rather than to other businesses. Hence, you may issue a simplified tax invoice showing the following:

Can I reclaim the VAT I pay on business purchases? Yes. As long as you have a Tax Invoice showing the VAT charged by your suppliers, and have paid for the goods or services concerned, you can reclaim the VAT on most of the goods and services you buy for your business. The sum of the tax amounts charged to you during a VAT accounting period will be the input tax that is declared on the tax return covering that period. Is there any input tax that I cannot reclaim? Yes. The VAT incurred on entertainment expenses, motor vehicles used for personal purposes and employee-related expenses cannot be reclaimed. What records will I need to keep? Records need to be kept for at least 5 years. You will have to keep:

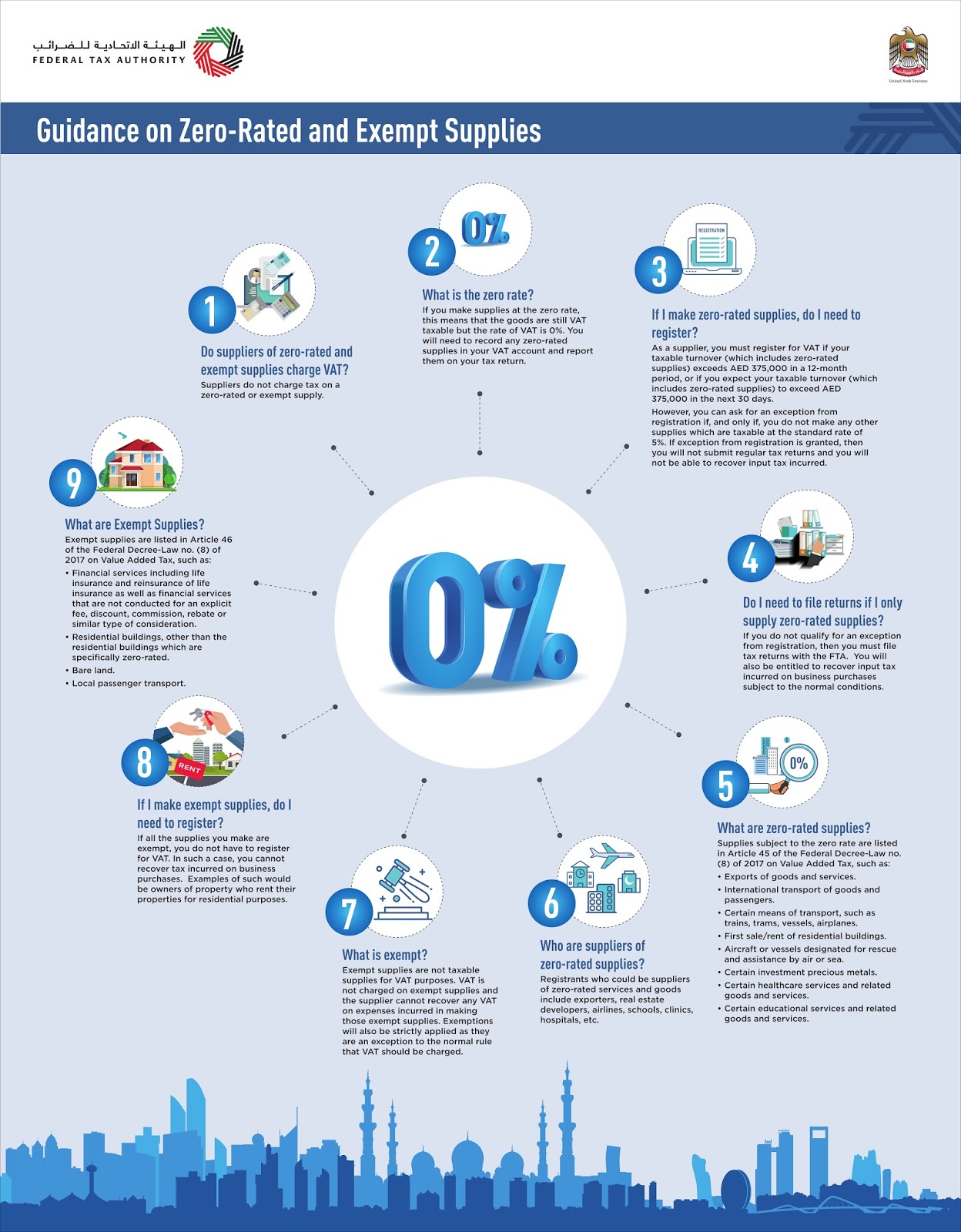

When and how will I file returns? You will normally be allocated a quarterly or monthly tax period according to your annual turnover, but the FTA may allow a shorter or longer tax period if it considers that to be appropriate. You will be required to file the tax return for each tax period by the 28th day of the month following the end of it (or on the next working day if the normal due date falls on a national holiday or weekend). Tax returns will be filed electronically through the FTA portal. When will I have to pay any tax due? You will be required to pay any tax due by the due date for each return – i.e. by the 28th day of the month following the end of each Tax Period (or on the next working day if the normal due date falls on a national holiday or weekend). When will I receive any repayment that I claim? Where you are in a repayment position, the FTA will inform you that any repayment claim that you make has been approved or rejected within 20 working days. On occasion, however, the FTA may inform you that consideration of the claim will take longer than that. What is the taxable amount? In relation to any given transaction, the amount that is subject to VAT is called the taxable amount. The taxable amount plus the tax is normally equivalent to the consideration for the supply i.e. the total amount received by the seller in return for supplying goods or services. The consideration will normally be in the form of money but in some cases the consideration may be partly or wholly non-monetary e.g. a voucher that has monetary value is one example of non-monetary consideration. How do I account for VAT on returned goods and refunds? If a customer returns an item and the retailer provides a refund then the retailer needs to issue a tax credit note and can reduce the output tax payable by reference to the amount of the refund. The output tax reduction should be made in the VAT accounting periods in which the refund is given. Do discounts and promotional offers alter the taxable amount? If a retailer offers a discount on the normal selling price of an item, or reduces prices in a seasonal sale for example, or perhaps offers “Buy One Get One Free”, then the reduced price actually paid by the customer is the consideration. How do I calculate the tax included in the consideration received from the customer? The VAT included in any price is equivalent to the consideration divided by 21. Source: https://www.tax.gov.ae/pdf/vat-retailers.pdf  Value-Added Tax or VAT is a tax on the consumption or use of goods and services levied at the point of sale. VAT is a form of indirect tax and is used in more than 180 countries around the world. The government of UAE published guidance on zero-rated and exempt supplies on their website (government.ae). Q.1: Do suppliers of zero-rated and exempt supplies charge VAT? Suppliers do not charge tax on a zero-rated or exempt supply. Q.2: What is the zero rate? If you make supplies at the zero rate, this means that the goods are still VAT taxable but the rate of VAT is 0%. You will need to record any zero-rated supplies in your VAT account and report them on your tax return. Q.3: If I make zero-rated supplies, do I need to register? As a supplier, you must register for VAT if your taxable turnover (which includes zero-rated supplies) exceeds AED 375,000 in a 12-month period, or if you expect your taxable turnover (which includes zero-rated supplies) to exceed AED 375,000 in the next 30 days.However, you can ask for an exception from registration if, and only if, you do not make any other supplies which are taxable at the standard rate of 5%. If exception from registration is granted, then you will not submit regular tax returns and you will not be able to recover input tax incurred. Q.4: Do I need to file returns if I only supply zero-rated supplies? If you do not qualify for an exception from registration, then you must file tax returns with the FTA. You will also be entitled to recover input tax incurred on business purchases subject to the normal conditions. Q.5: What are zero-rated supplies? Supplies subject to the zero rate are listed in Article 45 of the Federal Decree-Law no. (8) of 2017 on Value Added Tax, such as:

Q.6: Who are suppliers of zero-rated supplies? Registrants who could be suppliers of zero-rated services and goods include exporters, real estate developers, airlines, schools, clinics, hospitals, etc. Q.7: What is exempt? Exempt supplies are not taxable supplies for VAT purposes. VAT is not charged on exempt supplies and the supplier cannot recover any VAT on expenses incurred in making those exempt supplies. Exemptions will also be strictly applied as they are an exception to the normal rule that VAT should be charged. Q.8: If I make exempt supplies, do I need to register? If all the supplies you make are exempt, you do not have to register for VAT. In such a case, you cannot recover tax incurred on business purchases. Examples of such would be owners of property who rent their properties for residential purposes. Q.9: What are Exempt Supplies? Exempt supplies are listed in Article 46 of the Federal Decree-Law no. (8) of 2017 on Value Added Tax, such as:

Selected supplies in sectors such as transportation, real estate, financial services will be completely exempt from VAT The Federal Tax Authority (FTA) has announced the supplies that will be subject to Value Added Tax (VAT) as of January 1, 2018, revealing selected sectors that will be assigned zero-rated tax, such as education, healthcare, oil and gas, transportation and real estate. Selected supplies in sectors such as transportation, real estate, financial services will be completely exempt from VAT, whereas certain government activities will be outside the scope of the tax system (and, therefore, not subject to tax). These include activities that are solely carried out by the government with no competition with the private sector, activities carried out by non-profit organisations. The UAE Cabinet is expected to issue a Decision to identify the government bodies and non-profit organisations that are not subject to VAT. The below table outlines all supplies that will be subject to the 5% Value Added Tax, as well as zero-rated supplies and exempt supplies  VAT in UAE  Is it time for your business to implement an ERP platform? Business owners, executives, and other decision makers in every industry understand that adopting newer technologies like enterprise resource planning (ERP) is inherently beneficial, but such adoption will also require substantial investment. It is critical for businesses to clearly determine whether the benefits of ERP implementation outweigh the associated costs. Generally speaking, the larger and busier an organization is, the more worthwhile ERP adoption will be. But that just begs the question: how do you know your company is large and busy enough?

The question posed in the title of this article can be taken in two different ways. First, would the net benefit of implementing ERP now be sufficiently desirable? And second (if the answer to the first question is yes), at what specific time should ERP be implemented? Let’s take a closer look at both questions. To determine whether your business need is great enough, quickly evaluate your operations by asking yourself these questions:

Now let’s move on the second question: when is the right time to implement an ERP platform? While some experts suggest that organizations should wait for a period of stability (not during a hiring campaign, not while starting a new line of business, not during busy season, etc.), I don’t think that’s the right approach. If you decide to wait for ideal conditions, you’ll just keep on waiting forever. Here’s a better idea. Contact ERP implementation partners and find out how long it would take them to complete an implementation for you, along with how much it would cost. Then, compare this investment to the amount you are losing each year to inefficiency, late fees, lost opportunities, and so on. You will get a clear picture of how urgent your need is, how large a return on investment to expect from the ERP platform over the years, and how long it will take to recoup the cost of implementation. While some well-known ERP solutions take years to implement and cost millions or tens of millions of dollars, Microsoft Dynamics AX and the cloud-based Microsoft Dynamics 365 for Operations deploy more quickly for a fraction of the cost. In a recent study on ERP implementations in Saudi Arabia (Parveen & Maimani, 2014), Microsoft ERP solutions required the lowest levels of investment and resulted in the least operational disruption time during implementation. The authors also observed that Microsoft Dynamics was highly customizable, flexible, user-friendly, and open to integration. These characteristics make Microsoft Dynamics ERP solutions highly attractive for companies that want to improve efficiency without spending millions of dollars. Arguably the most important factors in reducing implementation time and remaining within budget are the industry-specific experience and technical competence of your ERP implementation partner. As a Microsoft Dynamics partner in Dubai, TechVista Systems possesses experience in implementing Microsoft Dynamics technologies on a large scale in many industries in the Middle East. Our client base includes major businesses in the public sector, banking, oil and gas, telecom, education, consumer goods, and other industries in the UAE and beyond. Please contact TechVista Systems to schedule a complimentary consultation and learn more about how we can help you improve efficiency and gain a competitive advantage with Microsoft Dynamics ERP solutions. References Parveen, M., & Maimani, K. (2014). A Comparative Study between the Different Sectors Using the ERP Software in Jeddah Region-KSA. Life Sci. J, 11, 40-45. Source: https://www.techvistasystems.com/blog/it-time-your-business-implement-erp-platform 11/14/2017 1 Comment TechVista Systems on 2018 strategies (L-R) Khurram Majeed, TechVista Systems and Philippe de Mazieres, Gulf Software Distribution (L-R) Khurram Majeed, TechVista Systems and Philippe de Mazieres, Gulf Software Distribution Khurram Majeed, general manager, TechVista Systems, shares details on its partnership with regional VAD Gulf Software Distribution and strategies for 2018. TechVista Systems, a subsidiary of Systems Limited, headquartered out of Pakistan, began its UAE business in 2014. With operations in UAE, Qatar and Australia, the software services provider has been working with regional value-added distributor, Gulf Software Distribution (GSD) since its inception in 2016. Khurram Majeed, general manager, TechVista Systems, says, “Before partnering with GSD, we were working with GBM for IBM technologies. However, we were still growing our footprint in these areas. We used to work excessively with IBM in Pakistan. Over the last year, we have aggressively started working with GSD and non-IBM platforms.” As a software services company, the reseller also has a huge presence in the US with Fortune 500 companies as customers. The firm decided to bring in the same portfolio of offerings into the region to replicate the success.

“We were working with IBM platforms and specific technologies in IBM, which are mainly towards business process automation, end-to-end integration with different systems, newer areas such as Robotic Process Automation (RPA) and machine learning,” he says. “We are mainly involved in business process automation, reengineering and optimisation part of the technology. We are also working with other principles such as Microsoft and MicroStrategy on different enterprise agreements and providing services on those platforms.” Majority of the reseller’s customers are from government and retail verticals. “We provide end-to-end retail solutions based on different technologies. We are not bound to a single vendor and have varied skillsets where we offer services on different technology areas for our customer.” According to Majeed, as the technologies they dealt with were emerging and as they were new to the region, the biggest advantage of partnering with GSD was that the distributor helped them penetrate the market. “GSD assists us to create our value proposition around these products. They work as a bridge between IBM and our firm. They also help us in developing our expertise, expanding our footprint, generating leads and marketing our portfolio,” Majeed adds. Philippe de Mazieres, general manager, Gulf Software Distribution, says, “TechVista’s solutions are more specific to enterprise and high-value. It is more about presenting the solutions as a value proposition rather than mass marketing. TechVista brings the expertise and experience in this domain and they bring that value to the customers.” Over the next few years, we will see the reseller increasing its focus on RPA solutions. Through artificial intelligence and machine learning capabilities, the software is able to carry out high-volume tasks that used to involve a human to complete it. “This technology is coming up and will make business processes much more efficient. We will be focusing on RPA in the future. This year, we are majorly focused on business process automation and building middleware solutions for big enterprises. And this year we have just begun our footprint with IBM and GSD,” Majeed says. “Next year we want to capitalise on that and extend our capabilities on the new things that are coming to the market. We will look at investing into these technologies and expand our footprint and our partnership with GSD and IBM with the new technologies.” Mazieres adds, “We will continue to invest in our channel to support them to bring the right value to the customers.” Find out more: https://issuu.com/resellerme/docs/251_rme_nov_2017/36 Source: http://www.tahawultech.com/resellerme/features/techvista-systems-2018-strategies/ “Service which is rendered without joy helps neither the servant nor the served. But all the other pleasures and possessions pale into nothingness before service which is rendered in a spirit of joy” Goodbyes are always very difficult and when it is not done in the right way, we end up in a puddle of trouble. Each one of us expects to conclude the service or rather called as the relationship with the employer in a smooth manner. Every employee must be aware about the facts of the benefits that one is entitled to; during the time of ending ones services. If you reside and work in UAE or run your own business here, then you must make yourself beaten by the Labour Laws present here. This helps you to get familiar with your rights and secure them. Before getting into the intense part of end of service benefits, let us have an understanding of the severance payment in UAE. According to UAE laws, end of service benefits otherwise known as gratuity, is defined as the sum of money that an employer is lawfully required to pay to its employees upon the conclusion of the employment relationship, subject to the employee fulfilling certain criteria set out in UAE Labour Laws. From past 40 years it has always been an important subject for the labour rights of the employees who are entitled to receive after rendering their services to their employers for number of years. The Federal law no 8 of 1980 of UAE focuses on the provisions regarding the end of service gratuity. So many questions pops up in the mind while calculating the gratuity for an employee -has the employee completed more than a year of its services, whether his contract is a limited contract or unlimited contract; if the employee has any debt with the employer, whether the employer has terminated the employee or the employee has resigned. Hence we have to take so many aspects into consideration in order to provide proper rights to an employee before we bid adieu. Basis on which gratuity is calculated: Without prejudice to what is stipulated by the policies, gratuity is calculated according to the employee’s last received basic wage before the employee was terminated. The gratuity calculation depends upon two main aspects A) in case if the employee resigns and B) in case if the employer terminates the employee’s employment. The provisions relating to the end of service benefits are stipulated in Articles 132 to 141 of the UAE Federal Law no 8 of 1980. The gratuity is calculated as A) 21 days wages for each year of the first five years B) 30 days wages for each additional year on condition that the total of the gratuity does not exceed the wages of two years. Days of absence from work without pay are not taken into consideration in calculating the length of service. How is gratuity calculated? Gratuity is calculated on an annual basis or part thereof provided that the employee has actually completed one year of employment or more with the employer. However, it is subject to certain exceptions based on the type of contract (limited or unlimited contract) and in the event the employment contract has been terminated by the employer or the employee has violated his obligations under the Law. Gratuity Calculation:If an employee resigns or is terminated within a period of less than one year then the employee is not entitled for any end of service gratuity. Article 132, Section 2 stipulates the End of service remuneration of the UAE Labour Law. This is applicable on both the types of contracts whether it is limited or unlimited. In order to have a clear picture, let us go through the gratuity calculation for each contract separately. Unlimited Contract:More than a year and less than three years of service in case of resignation: If an employee who has resigned with his service of more than a year and less than three years; is entitled for 1/3 of 21 days basic salary for each year of his service.

More than three years but less than five years in case of resignation: If an employee who has resigned with his service of more than three years and less than five years; is entitled for 2/3 of 21 days basic salary for each year of his service. More than five years: If an employee who has resigned with his service of more than five years; is entitled for 21 days basic salary for each year of his service and 30 days basic salary for all the years worked thereafter. More than a year and less than three years of service in case of termination: If an employee has been terminated from the employment with the service period more than a year but less than three years, then the employee is eligible for 21 days basic salary for each year worked. More than three years and less than five years of service in case of termination: If an employee has been terminated from the employment with the service period more than three years but less than five years, then the employee is eligible for 21 days basic salary for each year worked. More than five years: If an employee who has been terminated with his service of more than five years; is entitled for 21 days basic salary for each year of his service and 30 days basic salary for all the years worked thereafter. Benefits of being fired: This ends your agony about whether to stay or go; the company has decided for you. Even if you have been thinking to surcease, getting fired can be traumatic; especially when it has never happened to you before. It is like getting a hard kick which affects your steady income. Suddenly you are jobless with the infamy entails. Also one needs to be mentally prepared to answer the question of the HRs as why were we fired. However, this is a better option when you need the severance pay to prop up your financial pillow. UAE Labour Laws have some provisions to provide benefits to the employee when being terminated.

|